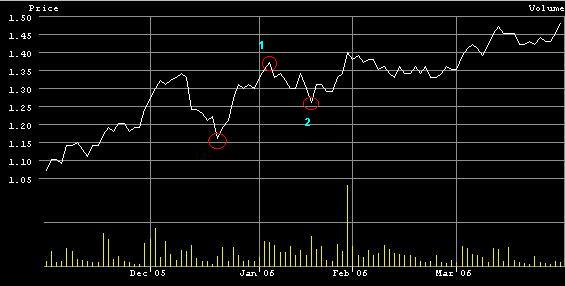

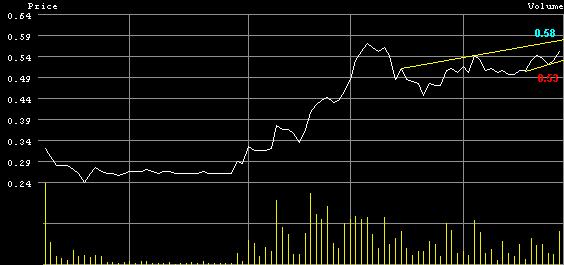

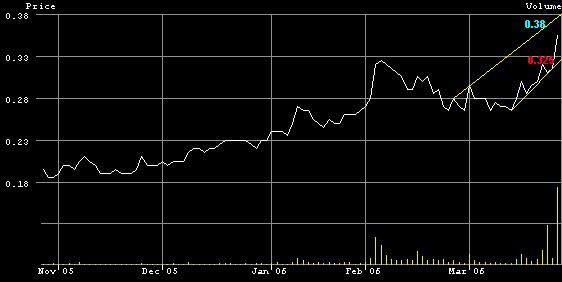

China Sun: Buy Call( Kim Eng)

♦ Ethanol plant construction hits some turbulence. CSBT restarted construction work on its Shenyang ethanol plant in mid-March following the winter break but has experienced unseasonably cold weather that intermittently interrupted work. It was reported on Xinhuanet that a week-long cold snap hit North and Northeast China in mid-March. Provinces such as Inner Mongolia, Heilongjiang, Jilin and Liaoning experienced lower than seasonal temperatures and heavy snowfall.

♦ But 2006 forecast maintained.

Management believes it can still begin trial production by June-July. The physical infrastructure is almost complete with only piping and ducts left to be installed. Machinery, once delivered, will take 2-3 months to install. While there is a possibility of delay, we are not adjusting our forecasts as we believe our assumption of 25% capacity utilisation for the full year is still appropriate.

♦ Business as usual.

Other than the above, it is business as usual for CSBT. Utilisation and sales mix of modified starch is stable, hence gross margin is likely to stay flat in 1Q06. However, utilisation of the newly added 200,000 tons of corn starch capacity in Tongliao has risen from 30% in 4Q05 to 50% currently. Assuming an ASP of RMB1,400 a ton for the additional output and net margin of 25% (FY05: 27.4%), another RMB14m in net profit should be added in 1Q06, which is inline with our full year forecast.

♦ Making headway in quest for fuel ethanol licence.

♦ But 2006 forecast maintained.

Management believes it can still begin trial production by June-July. The physical infrastructure is almost complete with only piping and ducts left to be installed. Machinery, once delivered, will take 2-3 months to install. While there is a possibility of delay, we are not adjusting our forecasts as we believe our assumption of 25% capacity utilisation for the full year is still appropriate.

♦ Business as usual.

Other than the above, it is business as usual for CSBT. Utilisation and sales mix of modified starch is stable, hence gross margin is likely to stay flat in 1Q06. However, utilisation of the newly added 200,000 tons of corn starch capacity in Tongliao has risen from 30% in 4Q05 to 50% currently. Assuming an ASP of RMB1,400 a ton for the additional output and net margin of 25% (FY05: 27.4%), another RMB14m in net profit should be added in 1Q06, which is inline with our full year forecast.

♦ Making headway in quest for fuel ethanol licence.

The recently concluded NPC did not firm up expectations for when the licence will be awarded. Only broad renewable energy statements were made by Chinese legislators, with no specific mention of ethanol. But CSBT’s gameplan to put itself forward as one of the desired candidates in the eyes of the central government may soon result in a joint venture or at least an MOU

for a partnership with one of the two major PRC oil companies.

♦ BUY maintained.

At S$0.695 currently, CSBT is valued at 8.4x 2006 EPS and 6.8x 2007 EPS. We believe these valuations are attractive relative to expected earnings growth of almost 30% in 2006 and a further 23% in 2007. Our DCF fair value (which excludes the fuel ethanol licence) is maintained at S$0.80 or 10x 2006

PE. Immediate comparable Global Bio-chem in HK trades at 12x forward PE.

for a partnership with one of the two major PRC oil companies.

♦ BUY maintained.

At S$0.695 currently, CSBT is valued at 8.4x 2006 EPS and 6.8x 2007 EPS. We believe these valuations are attractive relative to expected earnings growth of almost 30% in 2006 and a further 23% in 2007. Our DCF fair value (which excludes the fuel ethanol licence) is maintained at S$0.80 or 10x 2006

PE. Immediate comparable Global Bio-chem in HK trades at 12x forward PE.

posted by Bryan Chin @ 10:32:00 AM

0 comments

![]()